The Latest CBO Baseline and the Change in Tariff Policy

Weekly Lab Report – February 21, 2026

Fiscal Lab Notes is the official Substack page for the Fiscal Lab on Capitol Hill. You can check out all our work and analyses at fiscallab.org.

Last week, the Congressional Budget Office (CBO) released its latest Budget and Economic Outlook, which provides baseline projections for the federal budget and the broader economy, including deficits, debt, growth, interest rates, and labor market conditions.

Yesterday, the Supreme Court ruled the IEEPA tariffs unconstitutional. Because those tariffs comprised a large share of the Trump administration’s trade agenda, the decision would change key policy assumptions underlying the CBO baseline. The Fiscal Lab has analysis of both the baseline and the budgetary implications of the court’s ruling.

The CBO Baseline (Pre-Supreme Court Decision): A Grim Picture

Even before yesterday’s decision, the Budget and Economic Outlook looked grim.

In a short policy brief, senior fellows Patrick Horan and Joseph McCormack and project manager Michael Schultz review and analyze the main takeaways from the latest CBO baseline.

The federal government has a spending problem. In our policy brief, we agree with the CBO, which writes outlays, total deficits, net outlays for interest, and primary deficits are all “large by historical standards.” The latest baseline shows revenues modestly rising as a percentage of GDP, but outlays—primarily mandatory and net interest outlays—rising at a more rapid rate.

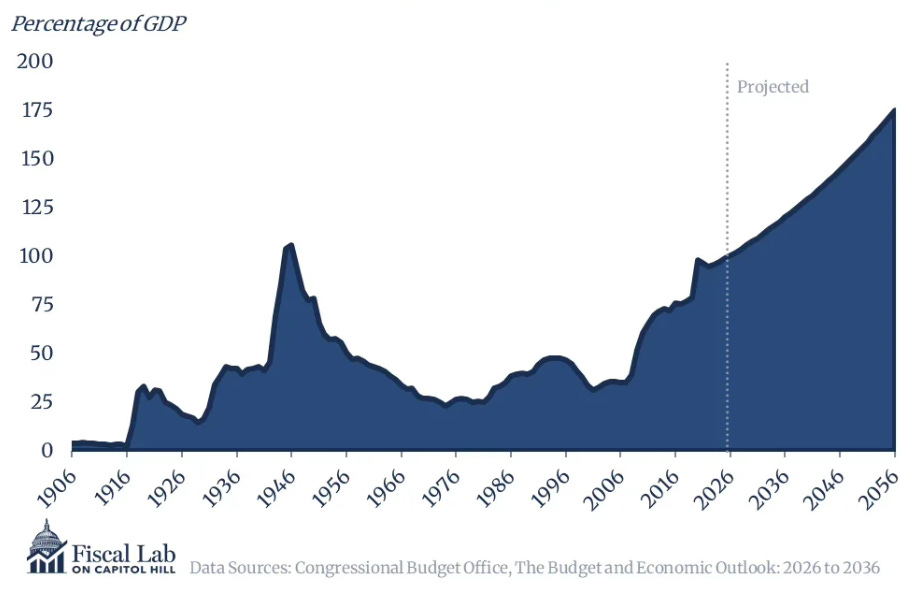

Large projected deficits will cause publicly held debt to GDP to rise to unprecedented levels in the coming years. The historical record for this metric is 106 percent in 1946, right after World War II. By 2036, publicly held debt to GDP will break this record and reach 120 percent (see Figure 1). Unlike in the postwar years though, the United States’ population is aging rapidly, meaning more pressure on Social Security and Medicare and fewer workers contributing to economic growth and generating tax revenue.

Figure 1: Federal Debt Held by the Public

The Budget Baseline (Post-Supreme Court Decision): An Even Grimmer Picture

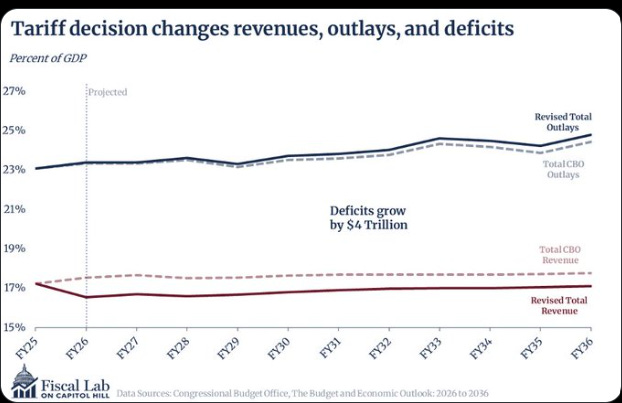

Although President Trump has issued an executive order imposing new tariffs in lieu of the court’s decision, the Fiscal Lab has conducted a quick analysis of what the ruling, by itself, means for the budget baseline. With no substitution, the end of the IEEPA tariffs would likely generate some economic growth as firms and individuals benefit from lower import prices. However, the reduction in tariff rates also means lower revenue, fueling larger primary deficits. Larger primary deficits, in turn, generate higher interest expenses. While economic growth can partially offset some of the increase in deficits through higher tax revenue, it will not offset all of it.

We find that, over 10 years, the Supreme Court decision:

· Reduces revenue by $3.1 trillion;

· Increases outlays by $948 billion; and

· Increases the federal deficit from $24.4 trillion to $24.8 trillion (see Figure 2).

Figure 2: How the Supreme Court Decision Affects the Budget Baseline

Uncertainty in the Baseline

Parker Sheppard also has a policy brief, observing that CBO does not fully explain the uncertainty around its projections. The baseline provides a point estimate for its variables. However, this point estimate is one path among many paths that are plausible.

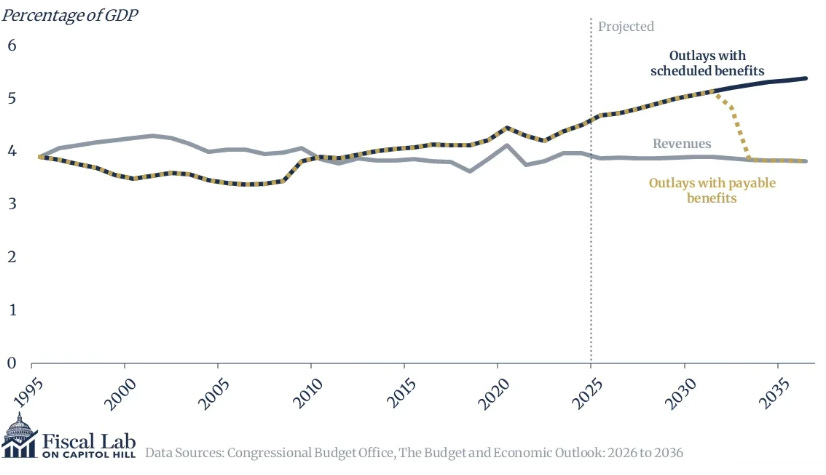

Sheppard explains different sources of uncertainty surrounding the baseline projections. One such source is incorporation of assumptions about certain policies that may not hold up in reality. For example, Social Security outlays are assumed to continue after its “trust fund is exhausted instead of being reduced to current revenues.” If the baseline did not have this assumption, outlays would fall by a substantial 28 percent in 2032 (see Figure 3).

Figure 3: Revenues and Outlays for Social Security with Scheduled and Payable Benefits

The CBO baseline should be viewed as a helpful starting point, but Congress should also be aware of the baseline’s confidence intervals. Publicly held debt to GDP is projected to reach 120 percent by 2036, but how likely is it to be higher or lower than that? Such information is crucial for Congress to make informed decisions as it considers how to budget appropriately.