The Fed Holds Steady, but Signals Rate Hikes Ahead

The Fed’s Shift Could Drive Up Federal Borrowing Costs

Fiscal Lab Notes is the official Substack page for the Fiscal Lab on Capitol Hill. You can check out all our work and analyses at fiscallab.org.

This week, the Federal Open Market Committee (FOMC), the Federal Reserve’s monetary policy decision-making body, voted unanimously to keep the federal funds rate at 3.5 percent to 3.75 percent. This decision, the first under new Chair Kevin Warsh, was in line with expectations as inflation is currently around four percent, well above the Fed’s two percent target, and unemployment is relatively low at 4.3 percent.

The FOMC also released its periodic Summary of Economic Projections (SEP) of participants’ projections for real GDP, unemployment, inflation, and the federal funds rate for this year and beyond. Notably, the median federal funds rate projection for 2026 was 3.8 percent, up from 3.4 percent in March. This change implies that the FOMC is expecting roughly one quarter percentage point (i.e., one typical rate change) increase before the end of the year, while it was expecting a quarter percentage point decrease in March. Although the median projection showed one increase, the “dot plot,” which shows all participants’ individual rate projections, showed six policymakers expecting multiple hikes.

The Federal Reserve has a congressional mandate to promote price stability and full employment. However, monetary policy changes affect Treasury debt service and our fiscal situation. The rates on T-bills, short-term Treasury bonds, closely track the federal funds rate. Apollo’s chief economist, Torsten Slok, recently observed that T-bills currently account for nearly 85 percent of gross Treasury issuance. Although the decision to keep the federal funds rate steady was no surprise, interest rates — and therefore debt-service costs — are now expected to be somewhat higher in the future.

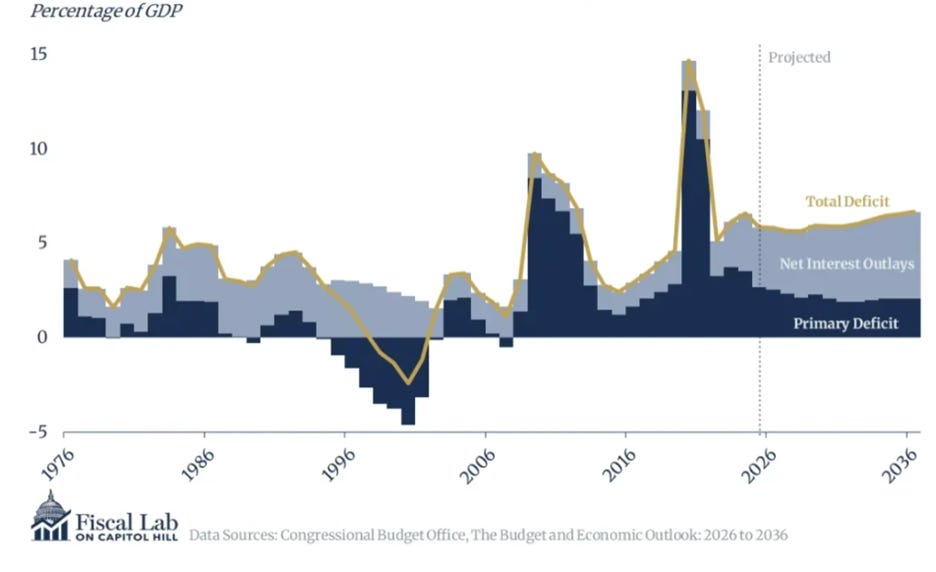

As my colleagues and I observed in February, net interest outlays have grown as a share of the budget deficit in recent years and are projected to grow even larger (see Figure 1).

Figure 1. Total Deficits, Net Outlays for Interest, Primary Deficits 1976-2036

If the Fed begins to increase the federal funds rate, this trend will worsen, especially as the large stock of debt issued at lower rates continues to mature and roll over at higher yields. (One major reason President Trump has argued for the Fed to lower its target interest rate is to lower government borrowing costs.)

Theoretically, by increasing relatively more longer-term bonds, the Treasury could increase the share of debt it can inflate away because those bonds would not have to be refinanced so quickly. However, this strategy also carries risk: markets pricing in higher future inflation would demand higher yields on longer-term bonds at issuance, which could worsen the very debt-service dynamics described above.

This week’s Fed decision underscores the relationship between monetary policy and the government’s borrowing costs. Although the decision was not a big surprise, it is a warning that if inflation remains elevated and further rate hikes are warranted, the federal budget will face increasing pressure.