Some Good Economic News and Returning to the Hamiltonian Norm

Weekly Lab Report – May 16, 2026

Fiscal Lab Notes is the official Substack page for the Fiscal Lab on Capitol Hill. You can check out all our work and analyses at fiscallab.org.

Strong Job Growth in April

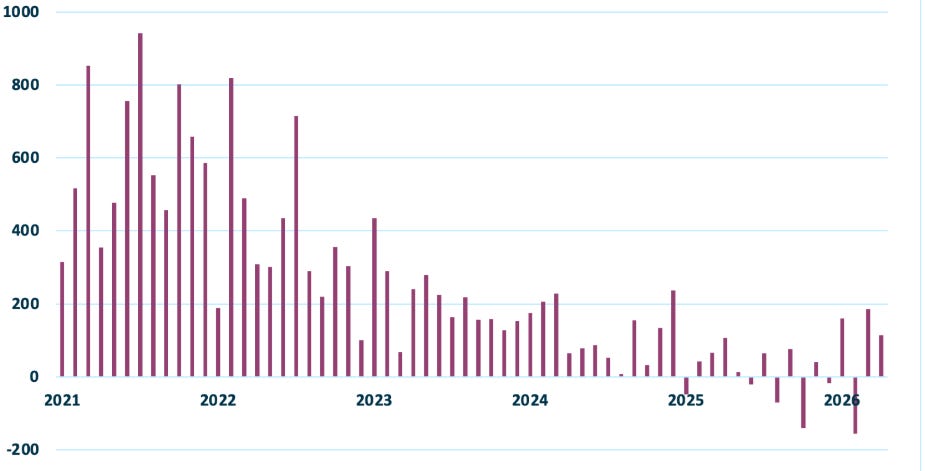

In his latest Economic Policy Innovation Center (EPIC) jobs report, Bill Beach argues the Bureau of Labor Statistics’ (BLS) April jobs report shows that US labor markets have been resilient in the face of war, rising prices, and a dramatic slowdown in migration. The BLS reports a net jobs gain of 115,000, well above economists’ consensus forecast of 55,000. Figure 1 shows much higher average monthly job growth in 2026 than in 2025.

Figure 1: Monthly Change in Total Non-Farm Payroll Employment, January 2021 through April 2026 (Thousands)

Source: Bureau of Labor Statistics, Economic Policy Innovation Center (EPIC)

The good news does not stop with the April jobs report. Beach also points to the latest BLS’ Job Openings and Labor Turnover report, which showed an increase in hiring from 4.9 million to 5.6 million in March. Hiring expanded in industries across the private sector, including Transportation, Warehousing, and Utilities; Professional Business services; and Leisure and Hospitality. In the first quarter of 2026, productivity also grew by a healthy 2.9 percent while final sales to private domestic purchasers, which measures output minus government consumption and inventories, grew at an impressive 2.5 percent.

Restoring Fiscal Rectitude

Earlier this week, Beach and Fiscal Lab board director, David Malpass, both submitted comments for a roundtable discussion, “Reducing America’s National Debt: Rooting Out Federal Waste, Fraud, and Overregulation,” hosted by the House Subcommittee on Economic Growth, Energy Policy, and Regulatory Affairs. Beach pointed to the importance of the “Hamiltonian norm,” the principle established by Alexander Hamilton that the United States would pay down its debt after short-term emergencies and not allow the debt to grow so large that it would threaten the value of the dollar. The Hamiltonian norm was established in the 1790s and was generally adhered to throughout much of US history, but Congress has largely ignored it in recent years as it has embraced chronic deficits.

To get our fiscal trajectory on the right track, Beach recommended a few immediate first steps. Social Security cost of living adjustments should be based on the CPI-U, the BLS’s official measure of price changes rather than the current CPI-W, which is an outdated metric. The criteria for means-tested programs should continue to be tightened. Drawing on research done with Parker Sheppard, he also recommended Congress establish a regulatory budget to limit the growth of federal regulations to boost economic growth.

Malpass similarly observed that the United States’ fiscal position is grim. Political will not solve the problem, so new checks and balances are needed. The United States has a debt limit, but it does not actually constrain spending. Rather, “[t]he current debt limit’s only concrete enforcement mechanism is a dangerous game of chicken over whether to default on Treasury debt, a step that would be monumentally damaging.” The next debt limit extension, which will happen next year, is an opportunity to replace this antiquated system with real enforcement mechanisms. Malpass argued “First, rather than default, there should be incremental consequences painful to Washington when it violates the debt limit. Second, the limit on spending or debt should be a percentage of gross domestic product rather than a dollar amount and should focus on cumulative debt, not annual deficits.” He also suggested several ideas for how to achieve the new debt limit including limiting executive branch spending and pay when debt is above the limit.

A New Fed Chair and the Fed’s Balance Sheet

On May 13, the Senate confirmed Kevin Warsh as the 17th chair of the Federal Reserve. Undoubtedly, Warsh faces many challenging issues, including stubbornly high inflation, messy labor market data, and Fed independence. Another major issue is the size of the Fed’s balance sheet, which has grown massively since the Great Financial Crisis. Warsh would like to aggressively reduce the balance sheet, which currently stands at approximately $6.73 trillion, and shrink the Fed’s footprint in financial markets.

Back in March, Sheppard wrote how a large Fed balance sheet blurs the distinction between monetary and fiscal policy. A larger balance sheet means greater potential for huge swings in profits as well as losses. The Fed’s QE program in response to the Covid-19 pandemic led to large losses, ultimately borne by taxpayers. The Fed has also blurred market signals by buying and holding trillions of dollars in Treasury debt. Without such large Fed intervention that lowers the yield on Treasury debt, markets would have likely forced more discipline on Congress.

Reducing the Fed’s balance sheet will be difficult and will also depend on fiscal reform that only Congress can deliver. The Fiscal Lab will have more to say about this in the coming weeks.