Budget Shocks, the Fed’s Balance Sheet, and Leprechaun Economics

Weekly Lab Report – March 21, 2026

Gone in 20 days: The CBO Baseline Meets SCOTUS and Operation Epic Fury

Last month, the Congressional Budget Office (CBO) published its latest baseline projections for the federal budget and the US economy. The budget baseline is important, in part, because it serves as the benchmark for how new legislation will affect the federal deficit. However, the baseline is a projection of federal spending and revenues under current law only.

We saw how brittle an assumption this is within days of the baseline coming out. Nine days later, the Supreme Court ruled President Trump’s authority to unilaterally enact tariffs under the International Emergency Economic Powers Act (IEEPA) unconstitutional. Another eight days later, the United States, along with Israel, began bombing Iran as part of Operation Epic Fury. Within 20 days, these two events have made the baseline obsolete as the Supreme Court ruling dramatically reduced expected revenues, while the war will almost certainly cause outlays to rise.

Bill Beach and Patrick Horan spoke about how these events will affect the federal budget as well as the broader economy. They also discussed how Congress and CBO could reform the baseline to take into account possible changes to policy.

The Challenges of a Large Fed Balance Sheet

Some politicians and commentators have recently criticized the Federal Reserve (Fed) for paying interest on reserves (IOR) as they view the policy as subsidizing banks at the cost of taxpayers. In a new policy brief, Parker Sheppard explains how that criticism identifies a real problem, but it “doesn’t address the underlying issue,” which is a large Fed balance sheet.

Prior to the 2008 Financial Crisis, the Fed had a comparatively small balance sheet and manipulated the federal funds rate through conventional open market operations where it bought and sold Treasury bills. In that crisis, the Fed made large-scale asset purchases and massively expanded its balance sheet to stabilize the banking system. To prevent those new reserves from creating excess inflation, the Fed began paying IOR to prevent banks from lending out those excess reserves into the economy.

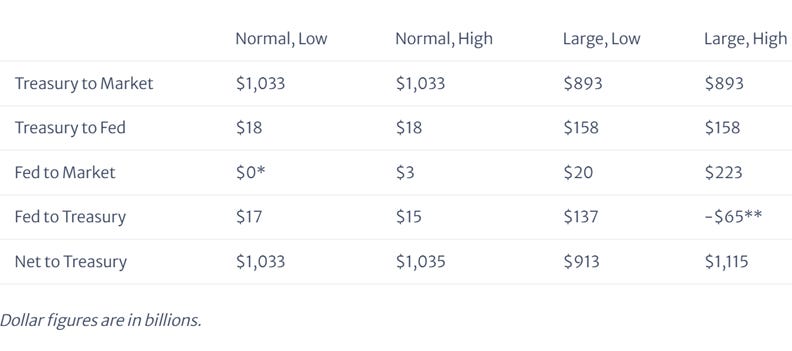

Sheppard explains how this arrangement blurs the distinction between fiscal and monetary policy and causes problems for the Fed. A large balance sheet where the Fed holds onto more Treasury assets causes the Fed to have a larger role in debt management, a role traditionally reserved for the Treasury Department. A large balance sheet also shifts fiscal risk to taxpayers when the Fed incurs losses on its balance sheet. Table 1 shows how interest earnings (positive or negative) flows between the public, the Fed, and Treasury depending on the size of the balance sheet and on the level of interest rates.

Table 1. Stylized interest flows

Sheppard argues for unwinding the Fed’s balance sheet, but to get there, Congress needs to help the Fed by reducing the federal deficit.

Can Leprechaun Gold Save Us?

Since St. Patrick’s Day was earlier this week, the Fiscal Lab decided to investigate the economics of leprechauns, the short elf-like creatures of Irish folklore. Legend tells us that leprechauns have pots of gold that can be found at the end of a rainbow.

How much leprechaun gold would be needed to pay off the federal debt? Assume a pot of leprechaun gold holds one cubic foot (a big pot). Now, let’s assume that big pot could contain 15,000 one-ounce gold coins. At a little over $5,000 per ounce (roughly the current price of gold), the pot would be worth just over $75 million. While that would be life-changing wealth for a household, it would only fund the federal government for about five minutes. To finance just one year’s deficit of roughly $1.85 trillion, it would take nearly 25,000 pots of gold. To pay off the entire US federal debt, now above $39 trillion, it would take nearly 520,000 pots.

That’s a lot of pots. And while leprechaun gold is mythical, it is an analogy for shortcuts that people try to find to bring themselves wealth. Many politicians try to find quick fixes to make our budget woes go away, but the real solution to our fiscal woes will be discipline and a willingness to make difficult policy decisions.